TravelingForMiles.com may receive commission from card issuers. Some or all of the card offers that appear on TravelingForMiles.com are from advertisers and may impact how and where card products appear on the site. TravelingForMiles.com does not include all card companies or all available card offers.

Other links to products and travel providers on this website will earn Traveling For Miles a commission that helps contribute to the running of the site. Opinions, reviews, analyses & recommendations are the author’s alone and have not been reviewed, endorsed, or approved by any of these entities. Terms apply to all credit card welcome offers, earning rates and benefits and some credit card benefits will require enrollment. For more details please see the disclosures found at the bottom of every page.

I hold considerably more credit cards than I can fit into my wallet, so only a few of my cards come with me wherever I go. Some cards have a home in my smartphone wallet but not my actual wallet, and some have to make do with a space in my desk drawer until such time that they’re called into action. One or two, however, never leave my side.

The Chase Sapphire Preferred® Card, lives in my smartphone and in my real-life wallet and that’s because it’s a card that works for me every day whether I’m home in LA, home in London, or traveling to some far-flung part of the world.

So, what is is about the Chase Sapphire Preferred® Card that I love so much?

The annual fee

The Chase Sapphire Preferred® Card costs $95/year and for a card that comes with all the benefits that this one does, that’s a low fee to pay.

Better yet, there’s no fee to add authorized users, so you can add someone to your account at no extra cost and they too can enjoy a lot of the card’s benefits while they earn you more points.

No foreign transaction fees

As someone who travels quite a lot, I like to know that I don’t have to worry that when I pull a card out of my wallet when outside of the US, it’s going to sting me for a fee when I use it to pay for a coffee, a meal, a taxi, or whatever else it may be that I’m buying, and that’s why the Chase Sapphire Preferred® Card never leaves my side.

Whether I’m home or traveling abroad, this card behaves in the same way and continues to offer its benefits and earning rates without adding on any fees.

3 points/dollar on worldwide dining

The Chase Sapphire Preferred® Card offers good earning rates in a variety of spending categories …

- 5 points/dollar on travel purchased through Chase Travel℠*.

- 5 points/dollar on Lyft rides (through March 2025) – link.

- 3 points/dollar on online grocery spending#.

- 3 points/dollar on select streaming services.

- 2 points/dollar on all travel that isn’t booked through Chase Travel℠^.

- 1 point/dollar for spending in all other categories.

… but it’s the earning rate on dining that I like the most.

No other Chase-issued credit card can beat the Chase Sapphire Preferred® Card when it comes to the earning rate on worldwide dining (not even the considerably more expensive Chase Sapphire Reserve®), and as it doesn’t charge foreign transaction fees, it is one of the most economical cards to use whether you’re dining at home or overseas.

*Hotel purchases that qualify for the $50 Anniversary Hotel Credit will not earn 5 points/dollar.

^Chase’s “travel” category is very broad, so you’ll earn 2 points per dollar on everything from airfare, rental cars, and hotel bookings through to car parking, tolls, and ride-sharing services.

#Excludes Target, Walmart, and wholesale clubs.

Ultimate Rewards partners

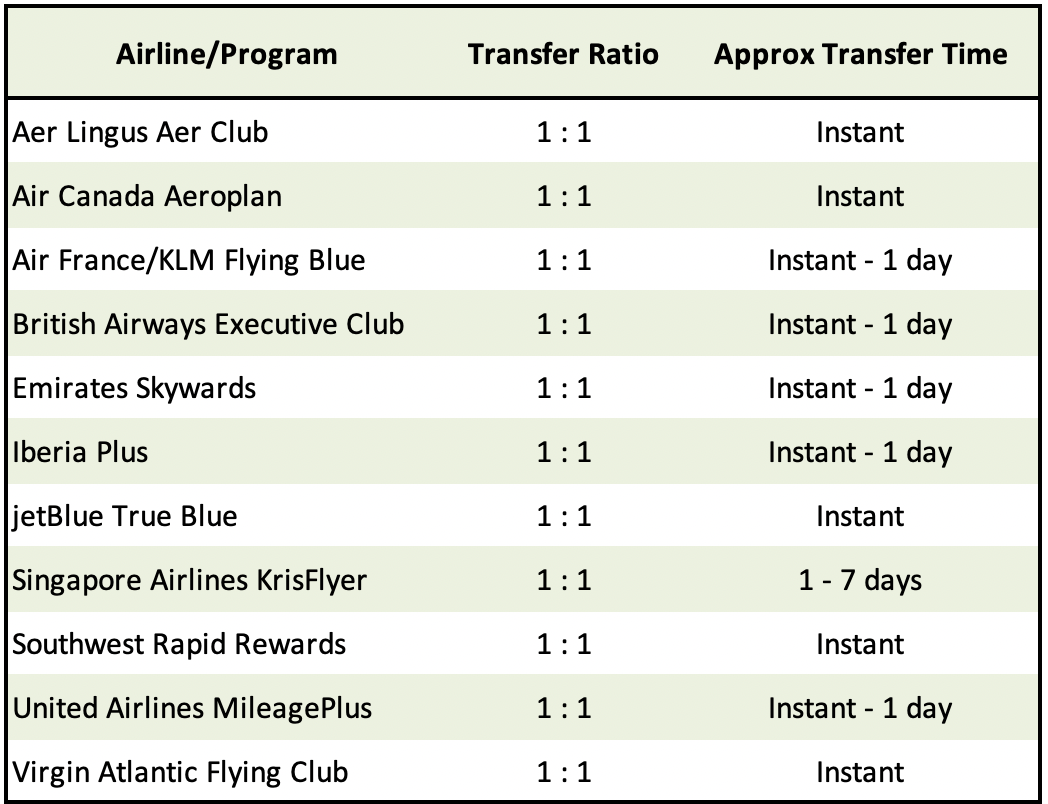

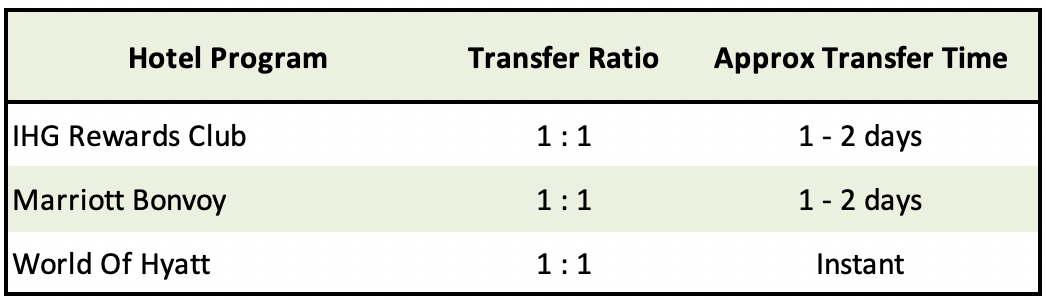

Ultimate Rewards partners with a variety of other airline and hotel loyalty programs (more details here), so the points that the Chase Sapphire Preferred® Card earns (which are Ultimate Rewards points) can be converted (in a 1:1 ratio) to programs like United’s MileagePlus, Singapore Airlines KrisFlyer, and the World of Hyatt, and this opens up a wide world of fantastic redemption opportunities.

Effectively, you can think of the the Chase Sapphire Preferred® Card as earning 1 to 5 points/miles per dollar in all of these loyalty programs:

Some points are more valuable than others, so not all transfer partners offer a great return, but when you have the Word of Hyatt as an option, you know that you’re always going to be able to get outsized value out of whatever the Chase Sapphire Preferred® Card earns you.

Chase Travel℠ bookings

Holders of this card use their points to book travel through the Chase Travel℠ portal with each point worth 1.25 cents towards whatever travel is booked.

The beauty of booking travel in this way is that a cardholder hands over points in exchange for a travel booking that Chase then books with cash, so there’s no need to search for award availability – all the airfares and hotels that are booked through the Chase Travel℠ portal are seen by the airline or hotel as cash bookings.

Flights booked through the Chase Travel℠ portal will earn frequent flyer miles/points and credits towards elite status, but because hotels view portal bookings as 3rd party bookings, hotel reservations made using Ultimate Rewards points will not qualify guests for loyalty program points/credits and elite status benefits are unlikely to be honored.

The welcome offer

At the time of writing, the card’s welcome offer looks like this:

Earn 60,000 bonus points after you spend $4,000 on purchases in the first 3 months from account opening. That’s $750 when you redeem through Chase Travel℠.

That’s not the best bonus that we have ever seen this card offer, but it’s still a very valuable one.

As the offer shows, if you redeem Ultimate Rewards through the Chase Travel℠ portal, you’ll get 1.25 cents of value out of each point and that makes the welcome bonus worth at least $750.

Personally, however, I know that I can get greater value out of my points by transferring them to Ultimate Rewards partners and then either booking high-end premium cabin flights or great hotels, and so for me, Ultimate Rewards are worth at least 1.5 cents each. That means that I value the welcome offer at an impressive $900.

The $50 hotel statement credit

Cardholders can earn up to $50 in statement credits each card anniversary year for hotel stays purchased through Chase Travel℠, and while this is a benefit best used when booking a stay at a boutique hotel, or at a hotel whose loyalty program you don’t value*, this can effectively cut the cost of holding the card by over 50%.

Personally, I use this when I need to book a 1-night stay at an airport hotel where I’m usually arriving too late and departing too early to care about elite benefits, and where the rate is low enough that the loyalty points that I’m giving up are irrelevant.

*Hotel bookings made through Chase will not earn points in a hotel’s loyalty program and will not be eligible for elite status benefits.

Security with a transferable currency

There’s no deadline by which you have to use or transfer over Ultimate Rewards points (they don’t expire), so you can hold any points you earn as an Ultimate Rewards balance until you know what program you’d like to use them in.

Then, when the timing is right for you, you simply transfer them across.

When you earn points in a single loyalty program (e.g. United MileagePlus) you’re limited to using those points through that one program only, and to make things worse, you’re also at the mercy of that one program – if (or when) that program devalues its currency, your balance devalues too.

By holding your points as a transferable currency like Ultimate Rewards, you limit your exposure to single program devaluations and you give yourself considerably more flexibility when it comes to how those points can be used.

Great primary rental car cover

The Chase Sapphire Preferred® Card gives cardholders primary rental car cover when they decline the rental company’s collision insurance and pay for the whole of their rental using their card.

As coverage is primary, there’s no need for a cardholder to get their own car insurance company involved in the case of an incident, and they can feel safe in the knowledge that the card’s coverage provides reimbursement up to the actual cash value of the vehicle for theft and collision.

Importantly, this protection covers most rental cars in the U.S. and abroad.

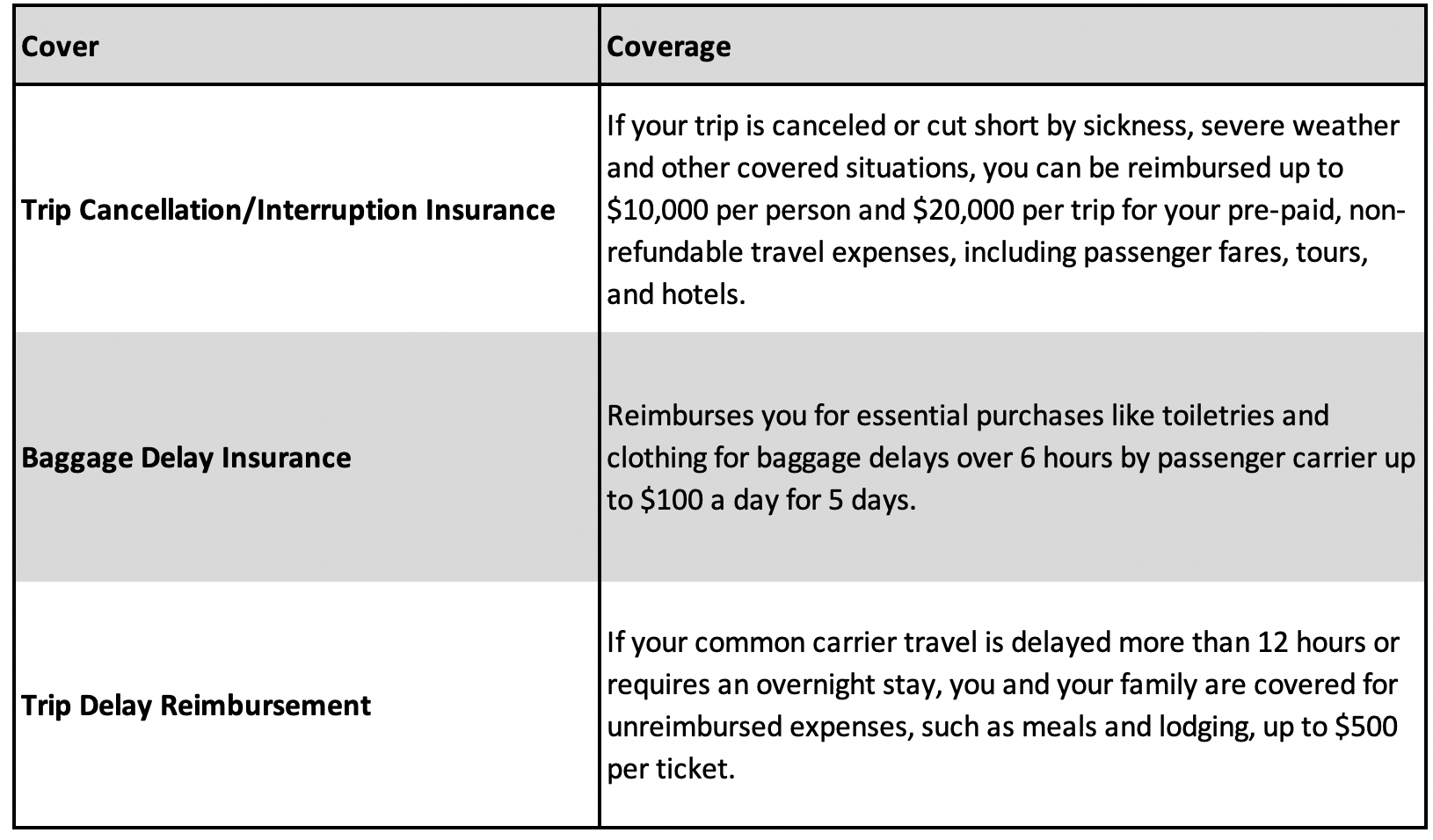

Soild trip protections & insurances

For a card that comes with an annual fee of just $95, the travel protections that it offers are pretty good.

This is what’s covered and how it’s covered:

When you consider that you can pay a lot more for a credit card and not receive any of those protections at all, this level of cover looks pretty good (although you’ll get even better cover with the Chase Sapphire Reserve® which, admittedly, costs considerably more to hold).

It makes other cards better

Not only is the Chase Sapphire Preferred® Card a great card in its own right, it also makes other cards even better than they already are.

Take these three very good cards as examples:

The Chase Freedom Flex® Credit Card comes with a $0 annual fee and, on its own, earns 5% cash back in rotating quarterly categories (on up to $1,500 in spending) and on travel purchased through Chase. It will also earn a cardholder 3% cash back on dining and on drugstore spending.

The Chase Freedom Unlimited® also comes with a $0 annual fee and, on its own, earns 5% cash back on travel purchased through Chase, 3% cash back on dining and on drugstore spending, and 1.5% cashback on spending in all other categories.

The Ink Business Cash® Credit Card comes with a $0 annual fee and, on its own, earns 5% cash back on the first $25,000 spent in combined purchases at office supply stores and on internet/cable/phone services. It also earns 2% cash back on the first $25,000 spent in combined purchases at gas stations and at restaurants.

When any (or all) of these cards are held by someone who also holds a Chase Sapphire Preferred® Card, all that cash back can be taken in the form of Ultimate Rewards points (1% cash back = 1 point) and that can result in fantastic returns on spending.

Someone holding a Chase Sapphire Preferred® Card and one of these cards as well, can earn a significant number of Ultimate Rewards points without much effort (that’s what I do).

Bottom line

I make no apologies for loving the Chase Sapphire Preferred® Card as much as I do because it’s a truly great card.

It’s a card that works well for people taking their first steps in the miles and points world and it’s a card that works for someone like me (a dinosaur who has been around the miles and points world for far too long).

It’s inexpensive to hold, it has good earning rates, it offers solid benefits, and because it earns one of the best currencies around, it offers cardholders a great deal of flexibility when it comes time for them to decide how they’d like to use those points.

Personally speaking, I can never have too many Ultimate Rewards points, and that’s why as I sit here typing this, the Chase Sapphire Preferred® Card is in my pocket ready to be used.

I’ll use it to pay for the rental car I’ll be picking up in a few days time, I’ll use it to pay for the dinner I’ll be eating later on, and I’ll use it to pay for my overpriced coffee tomorrow morning.

Best of all, I know that the points that the card earns me during the trip I’m currently on will go towards paying for the next great Hyatt stay that Joanna and I book, and by doing so, will save us a considerable amount of money.

That’s probably the biggest reason I love the Chase Sapphire Preferred® Card so much.

")

")

")

")