TravelingForMiles.com may receive commission from card issuers. Some or all of the card offers that appear on TravelingForMiles.com are from advertisers and may impact how and where card products appear on the site. TravelingForMiles.com does not include all card companies or all available card offers.

Some links to products and travel providers on this website will earn Traveling For Miles a commission which helps contribute to the running of the site – I’m very grateful to anyone who uses these links but their use is entirely optional. The compensation does not impact how and where products appear on this site and does not impact reviews that are published. For more details please see the advertising disclosure found at the bottom of every page.

I’m a very big fan of transferable currencies and that’s one of the reasons why I currently hold the three best known premium credit cards which between them cost me over $1,500 in annual fees.

The Platinum Card from American Express, the Chase Sapphire Reserve and the Citi Prestige card don’t actually cost me over $1,500 between them as they all offer me travel rebates that I use every year (although sometimes I come close to forgetting to use them!) and they all offer me benefits to which I can easily assign a monetary value….but I still have to justify holding three such expensive cards.

Last week I wrote a post reminding readers that, from 4 January 2019, some of the positive changes to the Citi Prestige card were kicking in (the negatives are coming later in the year) and reader “Lancelot” posted the following in the comments section:

“It seems your current strategy is to gain a ton of TY points. I’m interested to learn how you plan to use them.

My MR points & UR points are constantly used, but my thankyou points more/less sit there. I have the Citi Premier card and roughly 30K points currently banked. I moved 90K TY points to SQ for award travel about 6 months ago, so there’s that, but overall it still seems the ability to get value out of TY points (compared to MR & UR) is still a bit light. Am I missing something?”

There are a couple of interesting questions in there so I thought I’d use this post to address them and to explain how I’m planning to use the Citi Prestige card going forward.

First I’m going to cover a few basics upon which I can then build an explanation as to how I intend to get the best use out of my Citi prestige credit card.

Earning With The Citi Prestige Card

Since 4 January 2018 the Citi Prestige has seen its earnings in bonus categories improve. The card now offers the following:

- 5x ThankYou points at restaurants worldwide (up from 3x)

- 5x ThankYou points on air travel booked directly with an airline (up from 3x)

- 3x ThankYou points for spending with cruise lines (up from 1x)

- 3x ThankYou points for spending on hotels (no change)

- 2x ThankYou points on entertainment (through 31 August 2019 – then reverts to 1x)

- 1x ThankYou points on all other purchases (no change)

I value ThankYou points at a conservative 1.5 cents each (which is also the value I hold for Amex Membership Rewards points and Chase Ultimate Rewards points) so these earning rates make the Citi Prestige card a very strong proposition for anyone who spends a lot on airfare and dining.

Based on my valuations the Citi Prestige card offers an effective rebate of 7.5% at restaurants worldwide which no other card can match and, although the Platinum Card from American Express can match the effective rebate of 7.5% on airfare (when booking direct with an airline), the Citi Prestige offers better travel protection which makes it the more practical of the two cards to use when booking flights.

Citi ThankYou Transfer Partners

To fully understand how best to use the Citi Prestige card we have to look at two things:

1. The Citi ThankYou transfer partners

2. How Citi’s ThankYou transfer partners compare to the transfer partners of the other main transferable currencies

Everyone will have their own favorites here but, as far as I’m concerned, these are the transfer partners I value most:

- Air France/KLM FlyingBlue – for when there’s a good FlyingBlue Promo offer

- British Airways Executive Club – for short-haul redemptions

- Etihad Guest – for American Airlines awards (more details here)

- Singapore Airlines KrisFlyer – for aspirational long-haul awards

- World of Hyatt – for Andaz/Park Hyatt bookings

And it’s these partners that will dictate how I use all three of my premium credit cards going forward.

How I Plan To Use The Citi Prestige Card

You may have noticed that none of the transfer partners that I put in my list above are exclusive to Citi (some are not Citi ThankYou partners at all) and that goes a long way to explaining why my Citi Prestige card got very little use in 2018.

With Amex and Chase able to cover me for the main transfer partners that I value it was my Platinum Card from American Express (5 points/dollar on airfare) that I used for most of my flights (except in instances where I thought there was a risk of a missed connection or weather delays) and it was my Chase Sapphire Reserve Card that I used for dining (3 points/dollar) and for all other travel spending (3 points/dollar).

My Chase Prestige card only made an appearance when I wanted to use the 4th night free benefit and when I was making purchases that earned me bonus points for being in the “entertainment” category.

Thanks to the changes to the Citi Prestige earnings things will be different this year and this is how I plan to continue earning enough points to fund the transfer partners I value most:

- I’m happier earning 5 Citi ThankYou points per dollar spent on airfare and having travel delay/cancellation coverage than I am just earning 5 Membership Rewards points per dollar when I use my Platinum Card from American Express so I’m I’ll be using the Prestige card to purchase most of my flights.

- I’m moving my restaurant spending to the Citi Prestige card as it offers me a better return than the Chase Sapphire Reserve which was my card of choice for dining in 2018 (5 points/dollar vs 3 points/dollar).

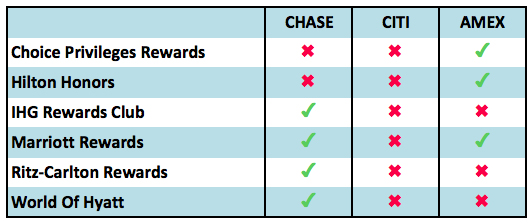

- I’ll continue to put most of my other travel spend on the Chase Sapphire Reserve card as the 3 points/dollar the card offers for all travel purchases keeps my Ultimate Rewards balance ticking over nicely (although I’ll continue use my Starwood Amex card for Marriott stays).

- As I will no longer be earning a significant number Membership Rewards points from the Platinum Card I’ll probably upgrade my Amex EveryDay card to the “Preferred” version to ensure that I increase my earnings on groceries (4.5 points/dollar on the first $6,000 spent).

I’m almost certainly going to earn a lot fewer Membership Rewards points this year but that shouldn’t be too much of an issue.

The Prestige Card will keep me covered for transfers to FlyingBlue, KrisFlyer and Etihad Guest and the Chase Sapphire Reserve will help me keep my British Airways Avios and World of Hyatt balances looking healthy.

To Sum Up

I don’t view my premium credit cards in isolation, instead I look at how they can work together to earn me as many points as possible towards the loyalty programs that I value most – I will happily use two or more transferable currencies to top up a single airline balance if that’s what works best for me.

That’s the overwhelming reason why I’m happy to split my earnings across the three major transferable currencies rather than concentrating on one or two and why I’m not focusing on just earning a ton of ThankYou points (as Lancelot thought I was) but concentrating on extracting as much value out of each card that I hold.

The beauty of transferable currency balances is that, unlike a lot of airline and hotel balances, you rarely face a situation where you have too few points to use effectively. As long as you have at least 1,000 points in a transferable currency you can use them to top up any number of other balances you hold.

Bottom Line

Before I heard the announcement of the changes to the Citi Prestige card earnings there was very little chance that I would keep the card past the end of last year but now it’s my Platinum Card that’s vulnerable to the chop.

The new earnings rates have given me a very good reason to put the Prestige card back in my wallet and the fact that I’m unlikely to use my Platinum Card for my airfare spending going forward means that it will now have to justify its position in my portfolio based on its travel benefits alone.

I’m not sure the Platinum Card can do that so I’ll be giving that a lot of thought….but that’s a topic for another time.

Any readers with any strong opinions (one way or the other) about the Citi Prestige card?

")

")

")

")

")

")

I think we agree that Citi may have salvaged this [pay a big fee and hope to breakeven] card; but it’s nowhere near what it was [“the best premium card ever”] when I signed up. Watch me run if I get a decent thank-you points transfer.

I think the value of the Prestige will vary widely depending on a people’s spending habits.

Someone who doesn’t really spend all the much on flights and/or dining is unlikely to get real value out of the card and will probably have trouble justifying having it in their portfolio. Someone who books a good few thousand dollars in airfare ever year and who eats out (or entertains out) often should easily be able to make this card work for them.

And yes, I agree, it’s not the card it was when if first came out…and that’s a shame.

[…] How I’m Incorporating The Citi Prestige Card Into My Spending […]