TravelingForMiles.com may receive commission from card issuers. Some or all of the card offers that appear on TravelingForMiles.com are from advertisers and may impact how and where card products appear on the site. TravelingForMiles.com does not include all card companies or all available card offers.

Some links to products and travel providers on this website will earn Traveling For Miles a commission that helps contribute to the running of the site. Traveling For Miles has partnered with CardRatings for our coverage of credit card products. Traveling For Miles and CardRatings may receive a commission from card issuers. Opinions, reviews, analyses & recommendations are the author’s alone and have not been reviewed, endorsed, or approved by any of these entities. Terms apply to all credit card welcome offers, earning rates and benefits and some credit card benefits will require enrollment. For more details please see the disclosures found at the bottom of every page.

Part way through last month, I mentioned that although I have never been the biggest fan of the card_name, my thinking had shifted slightly and I was now tempted to apply. Well, I took a couple more weeks to think things through and after deciding that the card would be a useful addition to my portfolio, I finally submitted an application last Friday. What happened since is an example of why you shouldn’t give up if an instant credit card approval isn’t forthcoming.

Background

Anyone who wants to know what the card_name offers can find out more about it in this earlier article, but before I continue, I’ll just give you a quick summary of why I didn’t really like the card when it was first released and what has changed in recent weeks.

If you’ve read the earlier article, you can jump ahead to the application section below.

Why I didn’t really like the card_name

- I already have card_name (the consumer card) so there was nothing in the business card’s earning rates that made me think that it’s a card I absolutely have to have.

- The benefits that the card offers didn’t wow me

When I’m not impressed with a credit card’s earnings rates and when its benefits don’t really impress me, that’s usually the end of things and it becomes a card that I know that I don’t want or need (until, possibly, the card gets refreshed).

However, the card_name hasn’t been refreshed, and yet here I am about to tell you about my short journey to getting approved for it.

What changed?

1 – The card started to offer something very interesting to new applicants

At the time of this particular application, the card_name was giving successful new applicants a chance to earn 60,000 bonus points when they spent $5,000 on their card in the first 3 months after opening their new account.

Also, and this is the interesting bit, the welcome offer went on to say that anyone who applied for the card by 6 October 2022 (and who was then approved), would earn double elite night credits on all eligible stays through to the end of the year.

As it looked like I was going to need all the help that I could get to requalify for Hyatt Globalist (top-tier) status, the double elite qualifying nights were valuable to me.

2 – I finally started to appreciate one of the card’s unique benefits

In the weeks leading up to my application, I had come to appreciate the Hyatt Leverage program (I discussed this program a few weeks ago) and while this is a program that anyone can join for at least a year, it’s also a program that you can be excluded from if you don’t spend at least 50 nights/year at Hyatt properties.

The card_name exempts cardholders from the 50-night requirement and as I had been saving quite a bit of money by using this program, I wanted to have an insurance policy in place that ensured that I didn’t lose access to the program in the future.

The application

After quite a bit of thought (because there are other Chase-issued credit cards that I’m also interested in getting), I decided that based on what the card_name could offer me, applying for it was a good idea.

I finally got around to submitting an application and I was immediately faced with a screen that said my application needed further review and that I’d hear back by mail within 10 business days.

This isn’t unusual in the world of Chase business card applications, but it’s always a lot nicer to get approved on the spot.

Aware that I wanted this card in my hands as quickly as possible and because I assumed that Chase probably wanted me to move some credit around (I have solid credit lines on two other Chase business cards), I called the number on the back of my card_name to see if I could get the review process fast-tracked.

The agent I spoke to was helpful and confirmed that he could see that my application was “pending review”, but because the “business lending division” had all gone home for the day, there wasn’t much that he could do.

The next day, I called back again and this time I got through to someone in the right department and quickly found out two things:

- My lines of credit didn’t have anything to do with the review (my offer to move some credit around was deemed unnecessary).

- The agent wasn’t prepared to tell me what the review was all about.

This didn’t bode well and my hopes of getting the card felt like they had disappeared completely when she told me that the review was going to have to be pushed up to a higher pay grade and that “I’d hear back within 10 business days”.

At this point, I was pretty sure that I would not be getting the card_name, and my mood wasn’t improved by the news that the person that my review had to go to wasn’t back in the office until after the weekend (so I couldn’t ask to speak to them there and then) – I guess even bankers need time off 😁.

Despite the fact that I felt there was more chance of me being declared the next Pope than there was of me now being approved for the card_name, I called Chase one final time on Monday afternoon.

Disappointingly and despite (somehow) managing to get to speak to the right person at the right pay grade, I was brushed off once again.

Apparently, “more work” needed to be done on the application before a final decision could be issued (how hard is it to say no??!!)

That was it.

At that point, I gave up and assumed that I’d get my rejection in the mail in the coming weeks. I wasn’t happy about it, but as this is part of living in the miles and points world, I didn’t have a problem with what I assumed Chase’s decision was.

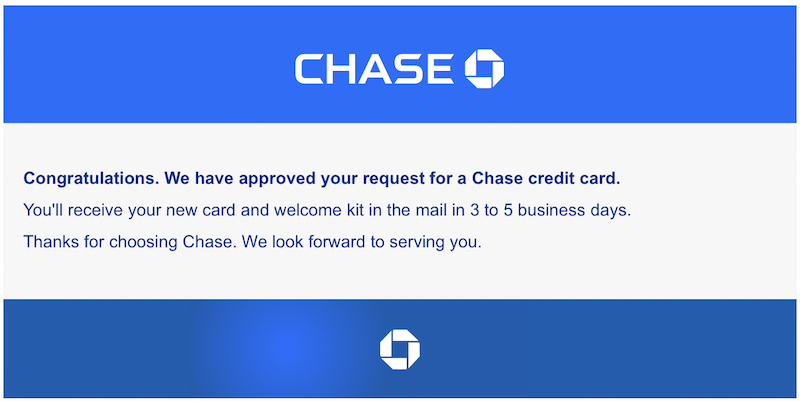

A few days later, as I was working away on my laptop, I saw an email from Chase drop into my inbox with the subject line “Thank you for your interest in a Chase credit card” and I assumed that the very next line within the body of the email would be something along the lines of “we have not been able to approve your application… etc…”

It wasn’t. Instead, this is what it said.

I was amazed.

After the conversations that I’d been having with the various phone agents, I genuinely didn’t think that I had any chance of being approved for the card_name and considering that this is a card that I’ve been quite disparaging about in the past, I was surprised at how happy I was to get it. Apparently, I was quite invested in this application!

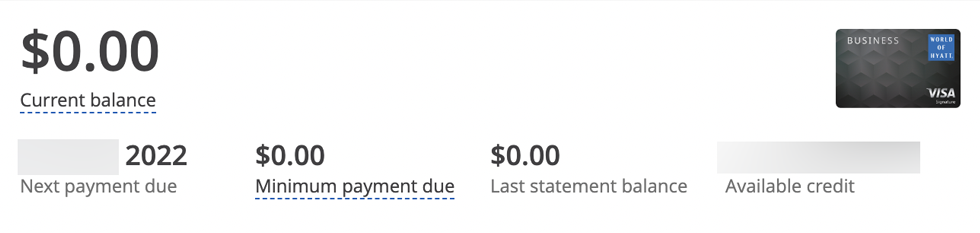

The card was quickly viewable in my online account (with a more than reasonable credit line)…

… and that led to me quickly booking a mattress run to make the most of the double elite night credits and to lock in Globalist status for another year. Happy days!

The moral of this story: Don’t write off a credit card completely until you’re really sure that it’s never going to offer you something that you value, and when you don’t get an instant credit card approval from Chase, don’t give up hope until you’ve got a rejection letter in your hands 😁

Featured image: The Andaz London courtesy of Hyatt

")

")

")

")

")

Had the sameresponse when I applied last Wednesday. But on Monday I signed into my Chase Business online account and saw the Hyatt card listed. Still no email confirmation, but hopefully will see the card soon.

Congratulations! What prompted you to apply?

appreciate this DP. but after being told so many times that additional review/time was required, they never told you WHY? and they just approved you? was this sol prop or EIN? no biz docs? no interrogation of your “business”?

personally, i dont like “higher” depts looking at my profile and getting eyes on my accounts for “further review”. this would concern me.

For this particular application, it was a sole prop which has a checking account with Chase. No information other than what I provided though the application process was requested.

nice. happy for you. awhile back, i got the CIP w/ EIN and required interrogation but no biz docs luckily. ive seen many DPs that sol prop was much easier.

also, i dont get why this card doesnt have free nite cert. not even spending $15k USD for free night like marriott. makes no sense. and no free EQN. you have to spend. so only the Hyatt Leverage is the key benefit.

I was 4 months away from being below 5/24 but was attracted to the 65K points I would receive once I completed the spending requirement so I took a chance and filled out the business card application. I received the congratulatory email that my application was accepted immediately rather than the expected “pending review” response.

In my state there is only 1 location, but when my wife and I did a 2 week road trip back in May, we would look at a list of hotels that we could redeem points at near the end of the day and many of those locales had Hyatt properties, many at 5K a night.

At a time of life where I will be able travel more, I’m looking to use points for free nights and Hyatt properties will help me achieve my goal.