TravelingForMiles.com may receive commission from card issuers. Some or all of the card offers that appear on TravelingForMiles.com are from advertisers and may impact how and where card products appear on the site. TravelingForMiles.com does not include all card companies or all available card offers.

Some links to products and travel providers on this website will earn Traveling For Miles a commission that helps contribute to the running of the site. Traveling For Miles has partnered with CardRatings for our coverage of credit card products. Traveling For Miles and CardRatings may receive a commission from card issuers. Opinions, reviews, analyses & recommendations are the author’s alone and have not been reviewed, endorsed, or approved by any of these entities. Terms apply to all credit card welcome offers, earning rates and benefits and some credit card benefits will require enrollment. For more details please see the disclosures found at the bottom of every page.

It was only yesterday that I was giving Chase a well-deserved hard time for altering credit card benefits without any advance warning and sometimes even without informing cardholders at all (cardholders are left to find out by chance or from the various blogs that write about this stuff… and that’s if they ever find out at all!) and now it seems that the card issuer has repeated the trick with another one of its credit cards… albeit a credit card that’s no longer open to new applicants.

The Ritz-Carlton Rewards credit card from Chase was closed to new applicants when Marriott merged with Starwood and Chase lost the right to issue Marriott’s premium credit cards (Amex now offers Marriott’s top-level credit card), but it lives in a considerable number of people’s wallets thanks to a few very nice benefits that the card offers:

For a $450 annual fee, the Ritz-Carlton Rewards credit card offers…

- An annual free night certificate (for properties costing up to 50,000 points/night)

- $300 in airline incidental fee credits annually

- $100 Ritz-Carlton/Marriott credit which can be used during paid stays of 2-nights or longer

- $100 Global Entry credit

- 3 club-level upgrades at Ritz-Carlton properties (on paid stays)

- Priority Pass Select Membership

- 15 elite night credits per year

- Marriott Bonvoy Gold status

- Marriott Bonvoy Platinum status after a cardholder spends $75,000 on the card in a year.

…as well as a number of solid travel insurance/protections that are only really matched by the card_name.

The Ritz-Carlton Rewards credit card also offers offered one of the best benefits out of any credit card around and that was the $100 Visa Infinite Airfare discount that cardholders could use every time they purchased two round-trip domestic flights on the same booking.

This benefit was open to all classes of bookings and wasn’t capped so, even though it couldn’t be used on low-cost carriers, cardholders traveling as a couple (or in a pair) could make substantial savings every year with this benefit alone. Not any more.

This was a benefit that was only offered (in the US) on very select Visa Infinite cards and we saw the CNB Crystal Visa Infinite card remove this benefit towards the end of last year. Now Chase has followed suit.

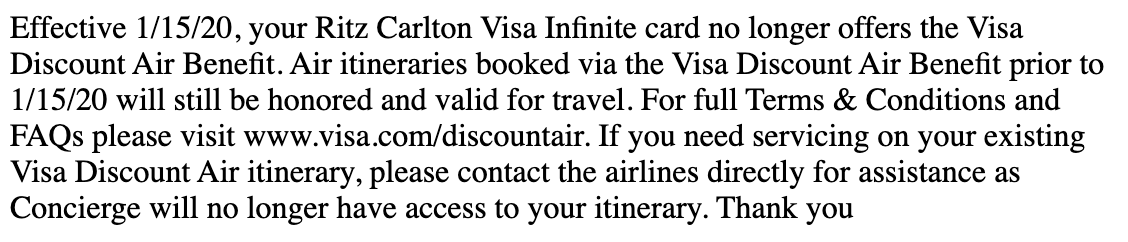

To make use of this benefit, cardholders had to make their bookings through a dedicated website portal but visitors to that portal now just see the following message when the page resolves:

That’s it. There’s nothing else on the page.

The issue

The problem here isn’t that Chase has removed a very valuable benefit from a card that costs $450/year (most people realized some time ago that this benefit was too good to last). The problem is that, once again, Chase has modified a benefit (in this case it removed it completely) without any warning and, as far as we can tell, without notifying cardholders in any way at all.

I don’t know of a single Ritz-Carlton Rewards cardholder who has received a letter/email from Chase to let them know that their $450/year credit card just lost a big benefit.

Why?!

Is it really too much to ask to expect a credit card issuer (especially one the size of Chase) to let customers know when something they’re paying for gets changed/downgraded? CNB managed it when they cut the Visa Infinite airfare benefit (they gave cardholders 2 month’s notice) so why not Chase?

Credit card companies are great at bombarding customers with emails, flyers, and letters reminding them of how fantastic their credit card benefits are, so why is it that when a benefit gets cut or downgraded it seems like the card issuers (notably Chase) act like they’ve forgotten how to contact anyone?

It’s unacceptable.

Bottom line

I’m not sure how it isn’t against the law for a credit card issuer to change the benefits of one of its cards without giving some advance notice (or at least informing cardholders after the fact) but apparently it isn’t, so Chase is making the most of this.

I’ve been a big fan of Chase and its credit card line-up for a very long time and I’ve been a big advocate for cards like the card_name, the card_name, and the card_name, but when Chase acts like this it leaves a very bad taste in the mouth.

There is no reason or excuse for Chase not to give cardholders advance warning when benefits are being downgraded (or eliminated completely) and the more times Chase acts this way the less faith cardholders will have in its products. Will anyone really blame them?

")

")

")

As a RC card holder, I can confirm that Chase offered me no warning and prior notice to the removal of this benefit. I am truly pissed and will likely consider cancelling this card now. While I travel frequently, I do not travel enough to earn either airline or hotel status. With Marriott’s downgrade of platinum status (which I earned through spent on the RC card for both Marriott status and the united Silver cross-status.

Now that Marriott status is worthless (gold is nearly as good as platinum) and the loss of this benefit, there really is no reason to keep this card.

Before complaining about Chase, did you try checking out the website in your post – visa.com/discountair? It looks to me that Visa has canceled the benefit as of 12/31/19 (as per that website) – so I’d believe that all Visa Infinite cards now have lost this feature.

Just because Visa was the one who pulled the plug on this doesn’t mean that Chase doesn’t have a responsibility to inform cardholders of the change.

Also, as it’s highly unlikely that Visa pulled the benefit without informing Chase in advance (doing that that would almost certainly go against whatever agreement Chase and Visa have) Chase has no excuse for not givving cardholders advance warning – CNB managed it.

It appears as though this was not a choice made by Chase and was actually a choice made by Visa.

You can see this on the Visa Infinite benefits page: https://usa.visa.com/pay-with-visa/cards/visa-credit-cards/discount-air.html

Looks like this benefit has been discontinued on all Visa Infinite cards and the Ritz was just the last to go. Shame they offered no notice but it’s definitely not 100% Chase.

Chase may not have removed the benefit (that wasn’t my issue anyway) but given that CNB managed to give all its cardholders 2 months warning that the benefit was going away you have to wonder why Chase didn’t bother to do the same (there’s absolutely no way that Chase didn’t know about this at the same time that CNB found out).

Did you look at the fine print of last month’s billing statement? It was probably there… that’s how they cover these things.

I don’t hold the card so I can’t physically check myself, but the people I know who have the card all say they have had no notice of this (and someone somewhere would have brought this to the attention of one or more bloggers had it appeared on a Chase statement in the past few months)

This was probably the #1 reason to keep the card… hopefully they will figure out a way to bring the benefit BACK (even if it’s a lesser benefit, $25 off per ticket up to 4 tickets?). This was a great way to encourage me to travel which then led to me booking Marriott hotels. It was a perfect benefit to encourage booking their hotels.

Called to ask them about it and told them I want to cancel the card. No retention was offered, and apparently you do not get any annual fee refunded from cancelling the card early. I am only half way through my cycle, so am eating 6 months of annual fee. Morally this is wrong, but what about legally? Can a card dangle some benefit and then remove it?

I don’t know what the law says about this but, while I fully agree that this is morally wrong, I doubt Chase would be acting this way if it was in breach of regulations.